Use Accounting Ratios to Stave Off Financial Problems

Does the mere mention of accounting ratios may put your teeth on edge, and bring back bad memories of Accounting 101? It shouldn’t as ratios can help your quickly determine how your business compares against others.

Banks often use ratios to analyze your financial statements as part of the loan approval process, so it’s helpful to know in advance how you’ll be measured. Even better, ratios allow you to compare your business against your peers since many trade groups publish lists of average ratios within an industry.

Although ratios may have made you drowsy during accounting class, they can be a fascinating way to measure your company’s financial performance.

Gross Profit Margin

Simply put, gross profit margin-sometimes referred to as gross margin-is your revenues less your cost of sales. For some industries, this is a very meaningful metric, while it won’t mean as much to others. For instance, manufacturers, restaurants, and retailers often treat gross profit as a key performance indicator.

In such environments, one typically purchases inventory at one price, and ideally sells it to someone else at a higher price. The spread between these two numbers is the gross profit margin.

Let’s say that you buy $40 of pine straw (we’re trying to avoid the accounting class term widget) and sell it for $60. In this case, $20 of gross margin divided by $60 of sales yields a gross margin percentage of 33%. Thus one-third of your sales are available to put toward overhead items, such as office supplies, payroll, rent, taxes, and so on.

Ideally your gross margin is high enough to cover your overhead and leave you with a profit. With that example in mind, let’s see how you can calculate your own gross profit margin.

Caveat: Gross profit margin isn’t meaningful to everyone. For instance, if you’re a self-employed service provider, you may not have any cost of sales.

Your salary is arguably all or most of your profit. You can certainly count your salary as cost of sales and compute a gross profit margin, but you might not find much value in the result.

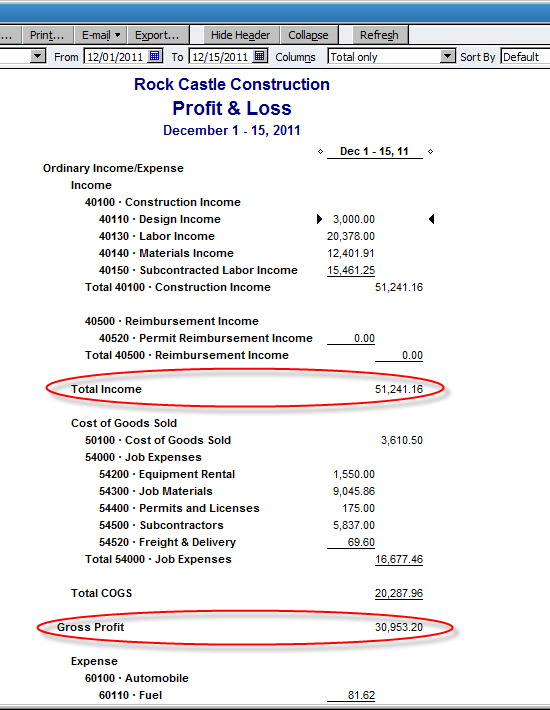

To begin, choose Reports, Company and Financial, and then Profit & Loss Standard. As shown in Figure 1, look for the Gross Profit amount, and then divide this by Total Income.

Figure 1: The Profit and Loss Standard report provides the figures you need to calculate gross profit.

In this case, $30,953.20/$51,241.16 shows a gross profit margin of 60.4%. Is that good? Is it bad? Very often the answer is “it depends”, which is why you should try to compare yourself to similar companies in your industry.

However, let’s consider the restaurant industry. Many owners strive to keep their gross margin at around 63%, which means a cost of goods sold percentage of 37%. The gross profit ratio enables you to track this key measurement, but you must ensure that your transactions are being recorded in the proper accounts.

The percentages can skew if, let’s say a telephone bill, is miscoded to Food Costs, instead of Telephone. Similarly, your cost of goods sold might look great only because someone miscoded food costs into an overhead account, such as Supplies.

Profit Margin

Profit margin is another commonly used ratio that you can derive from the Profit & Loss Standard report by dividing Net Income by Total Income. In essence, this is the percentage of sales that the owner of a business gets to keep-before Uncle Sam gets his share. Profit margins vary widely by industry.

For example, a grocery store chain may have profits of $2 billion, but a profit margin of just 2.6%. An oil company may have staggering profits in dollars, but their profit margin is often just 10%. Conversely, some software companies have a profit margin of 28% or more.

As with gross profit, the best way to determine whether a profit margin is reasonable is by comparing the result to one’s peers. The construction company shown in Figure 1 has Net Income for the period of $13,123.48, which when divided by Total Income of $51,241.16 returns a profit margin of 25.6%.

Inventory Turnover Ratio

This ratio illustrates how many times a year that you’re selling your entire inventory. This can help you gauge whether you may be holding too much inventory, or not enough. This ratio is based on cost of goods sold divided by average inventory.

As you’ve seen, cost of goods sold appears on the Profit and Loss Standard report-look for Total COGS-but you’ll have to perform a quick calculation to determine average inventory. To do so, divide the sum of your beginning inventory plus ending inventory by 2.

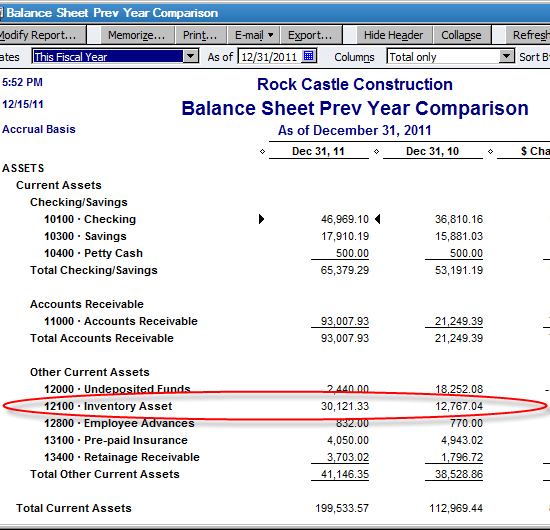

Although you can use several different reports in QuickBooks to determine the beginning and ending balance of your inventory, try this first: choose Reports, Company and Financial, and then Balance Sheet Prev Year Comparison.

Change the report date to This Fiscal Year, and then look for the inventory account balance, as shown in Figure 2.The ending balance for last year is also the beginning balance for this year.

If you need beginning and ending balances for a shorter period, such as a quarter, choose Reports, Accountant and Taxes, and then General Ledger. Set the report dates to the period of your choice, and then use the beginning and ending balances for your inventory account.

Figure 2: The Balance Sheet Prev Year Comparison can provide beginning and ending inventory balances.

Average Collection Period

This ratio helps you determine how long it takes your customers to pay their invoices. The formula is a little more complex than some of the other ratios: number of days multiplied by average accounts receivable balance, divided by credit sales.

For instance, let’s say that your average accounts receivable balance is $30,000, and you had total sales of$400,000 for the year. 365 multiplied by 30,000 is 10,950,000. This amount divided by our total sales of $400,000 is 27.38, meaning that on average your customers pay their invoice in just under 30 days.

Be sure to monitor your average collection period, as your cash flow can tighten quickly if that ratio increases. If you typically invoice your customers, then you can use the Total Income figure from your Profit & Loss Standard report.

Keep in mind: Average collection period won’t be of interest if your customers pay on the spot, such as in a retail store or restaurant.

Although QuickBooks doesn’t directly provide a figure for average accounts receivable, you can quickly customize a report to aid in this calculation:

- Choose Reports, Company and Financial, and then Balance Sheet Standard.

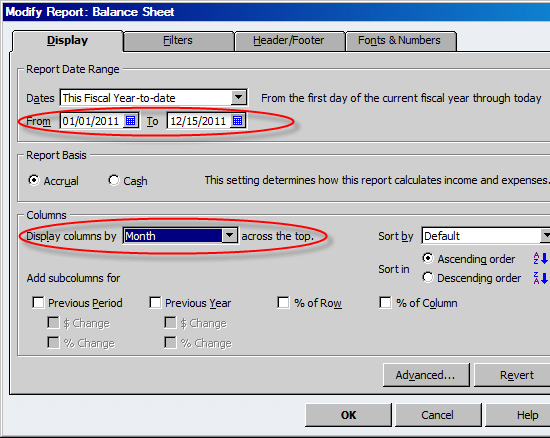

- Click the Modify report button, and then set the From and To dates to match the period shown on your Profit & Loss report. As shown in Figure 3, change the Display Columns By to Months, and then click OK.

Figure 3: Change Display Columns By to Months when you want a month-by-month report.

When QuickBooks displays the 12-month report, as shown in Figure 4, click the Export button, and then click OK to send the report to Microsoft Excel.

Figure 4: You can convert the Balance Sheet Standard report into a twelve-month format.

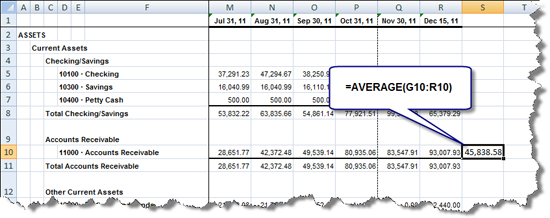

As shown in Figure 5, row 9 contains the Accounts Receivable figures. In cell R9, enter this formula to calculate your average accounts receivable balance: =AVERAGE(F9:R9).

Figure 5: Use the Accounts Receivable figures to calculate your average accounts receivable balance.

As you can see, the average collection period ratio enables you to determine how long it takes your customers to honor your invoices, which in turn has a direct impact on your cash flow.

Other Common Ratios

Current Ratio: Divide current assets by current liabilities to determine a firm’s liquidity.

Quick Ratio: Subtract inventory from current assets, and then divide by current liabilities to apply a more severe liquidity measurement.

Debt Ratio: Divide total debt by total assets to determine how much of the company is financed by debt.

Return On Assets: Banks often add net income plus interest expense together, and then divide this by total assets to determine the firm’s return on assets. This figure typically needs to exceed the interest rate of a loan that you may be contemplating.

Compare Yourself to Others

Now that you understand how to calculate ratios based on your financial results, the next step is to compare yourself to your peers. You may belong to a trade group that makes benchmarks available to its members. If not, a good first step is the BizStats web site, at www.bizstats.com.

Your line of business may be included in their free offerings, but even more information is available on a subscription basis. You can find even more resources by searching the Internet search for the term “industry benchmarks”.

Did You Know?

You can send your thoughts about QuickBooks to Intuit directly from within QuickBooks. To do so, choose Help, Send Feedback Online, and then one of these choices:

- Product Suggestion, as shown in Figure 6

- Bug Report

- Help System Suggestion

Any of these links will display an online from in your web browser so that you can submit your thoughts directly to the QuickBooks development team. QuickBooks frequently updates its products, so before you send a bug report, choose Help, and then Update QuickBooks. Click the Update Now button to ensure that you have the latest patches and fixes for your version of QuickBooks.

Figure 6: Submit your wish-list items directly to the development team from within QuickBooks.